When you’re considering jewelry insurance vs homeowners insurance, the big difference is that specialty jewelry insurance usually offers broader, item-specific protection, while a standard homeowners policy often will not cover loss or accidental damage, may have additional coverage limits or caps, and may require a deductible.

As such, when deciding between stand-alone jewelry insurance vs a homeowners floater, for expensive engagement or wedding rings, watches, and other high-value pieces, specialty jewelry insurance is often the better choice, as it provides clearer terms, higher limits, and protection designed specifically for the way jewelry is actually worn, stored, and lost.

We’re breaking down everything you need to know about jewelry coverage on a homeowners policy and the alternatives. Let’s take a look at your various options, and consider the pros and cons of each, as well as which option is going to be ideal for your unique circumstances.

What You Will Learn

- What Is the Difference Between a Homeowners (HO) Standard, Rider or Floater Policy?

- Is Stand-Alone Jewelry Insurance or a Homeowners Rider or Floater Better?

- Stand-Alone Jewelry Insurance vs Homeowners Rider or Floater Comparison

- Does a Homeowners Insurance Floater Cover Jewelry?

- What Does a Homeowners Insurance Floater or Rider Not Cover?

- How Limited Is Standard Homeowners Insurance for Jewelry?

- What Are the Hidden Costs of Putting Jewelry on Your Homeowners Policy?

- Will a Floater Claim Raise Your Homeowners Premium or Risk Nonrenewal?

- What Are the Advantages of Stand-Alone Jewelry Insurance?

- What Does Stand-Alone Jewelry Insurance Cover That a Rider or Floater Often Does Not?

- Jewelry Insurance vs. Homeowners Floater FAQs

What Is the Difference Between a Homeowners (HO) Standard, Rider or Floater Policy?

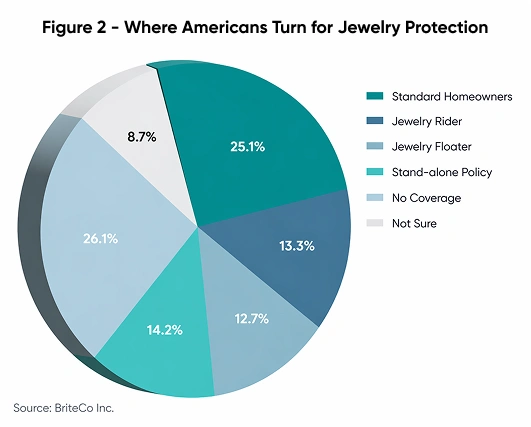

A standard homeowners policy usually includes personal items coverage that would include personal jewelry items. However, these policies are typically limited to a total of $1,500 to $2,000. For people with more valuable jewelry items, a jewelry rider can be added to a homeowners policy as an endorsement, which is an amendment to the homeowners policy that raises limits or broadens coverage for a category of property such as jewelry. The jewelry rider is often still tied to the homeowners policy’s original terms and deductible structure.

A jewelry floater is separate, scheduled coverage for specific expensive jewelry items such as an engagement ring, or a luxury watch, listed according to its individual value. Floaters are often written on broader “all‑risk” terms and can encompass no or a lower deductible. Jewelry floaters are commonly issued as an endorsement or companion inland marine policy by the same insurance company that writes the homeowners policy, with the floater “tied” to that home account. Many major homeowners insurance carriers will require you to carry a home or renters insurance policy with them to qualify for their jewelry floater policies.

Stand-alone policies offer coverage from a specialty jewelry provider that has coverage specifically designed for higher value jewelry items.

Is Stand-Alone Jewelry Insurance or a Homeowners Rider or Floater Better?

Stand-alone jewelry insurance is generally best if you have a high-value jewelry collection or if you want to avoid negatively impacting your insurance premiums after a claim (just note that BriteCo is currently the only specialty jewelry insurance provider that specifically states it does not report claims to CLUE or A-plus which are loss-history data services, thereby avoiding any impact on your homeowners policy). A homeowners rider or floater may suit those with valuable jewelry collections but likely risks an impact on a homeowners policy if a jewelry claim is made.

Stand-Alone Jewelry Insurance vs. Homeowners Rider/Floater Pros & Cons

| Insurance Type | Pros | Cons |

|---|---|---|

| Stand-Alone Jewelry Insurance |

|

|

| Existing Homeowners Policy (Rider/Floater) |

|

|

“A specialized jewelry insurance policy typically offers better rates and stronger coverage,” says Briteco Chief Actuary Conor Redmond. “You’ll be working with experts every step of the policy lifecycle, which is especially important if a claim arises. It means expedient replacement with true like kind and quality.”

Keep reading to learn more about specialty stand-alone jewelry vs. homeowners insurance jewelry coverage, and what you can expect from both, so you can make the best choice for your needs.

Stand-Alone Jewelry Insurance vs Homeowners Rider or Floater Comparison

Compare your jewelry insurance coverage options and all the need-to-know details, side by side.

| Coverage Feature | Stand-Alone Jewelry Insurance | Homeowners / Renters Insurance (Standard, Rider, or Floater) |

|---|---|---|

| Policy Type | Stand-alone, specialized jewelry insurance | Add-on to homeowners or renters policy as rider or floater |

| Claims Reporting – Impact on Home Insurance | Some stand-alone jewelry insurance companies report. BriteCo does not report to loss-history data services such as CLUE or A-PLUS. | Jewelry claims count against your home policy and claims history |

| Risk of HO Premium Increase or Non-Renewal | No risk with BriteCo stand-alone insurance. May be possible with others. | Possible HO premium increases, or non-renewals from a jewelry claim |

| Deductible | Various deductibles but zero on standard policies with BriteCo | Subject to homeowners deductible ($500–$2,500+ is common) |

| Coverage Type | Often all-risk coverage | Often named-peril or limited all-risk |

| Mysterious Disappearance | Often covered | Often excluded or limited |

| Natural Disasters | Often covered, including hurricanes and earthquakes | May be excluded depending on policy and location |

| Replacement Value | Repair or replacement at insured value. BriteCo policies provide 125% coverage replacement for insured value. | May only pay the depreciated actual cash value |

| Choice of Jeweler | You can typically work with your trusted jeweler for replacement/repair | Insurer often selects the replacement jeweler |

| Who Is Covered | The policyholder may add a spouse, partner, or fiancée | Typically limited to spouse or immediate family |

| Ease of Adding a Partner | Simple, online entry — no disruption in coverage with BriteCo | May require policy changes or additional underwriting |

| Security Device Discounts | May provide discounts for home safes and alarm systems | Often there are no jewelry-specific discounts |

| Best For | High-value, frequently worn jewelry | Low-value items or minimal coverage needs |

| Policy Maintenance | Automatic value updates as metal and gem prices rise with BriteCo | Appraisals often outdated unless manually updated |

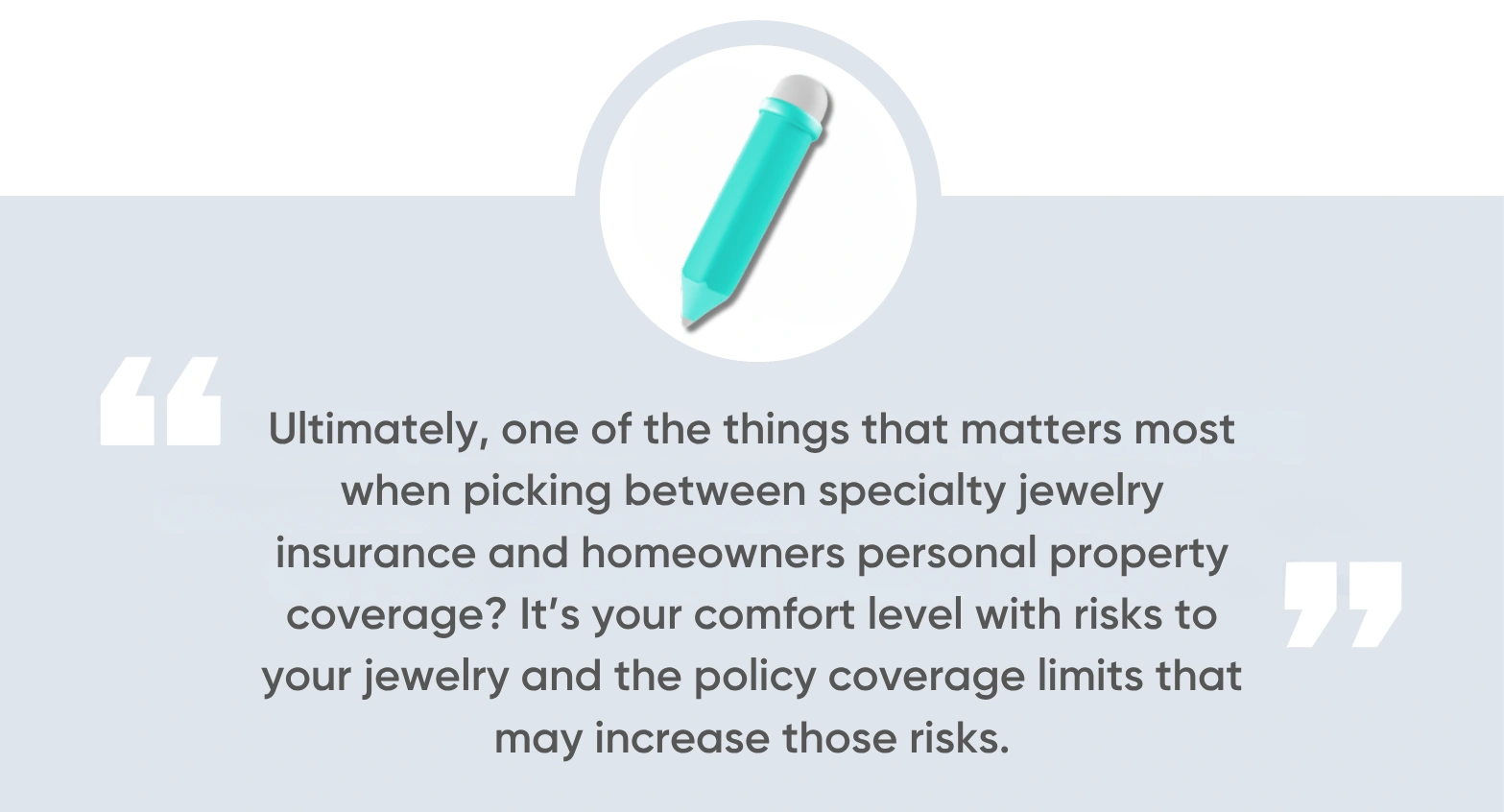

Ultimately, one of the things that matters most when picking between specialty jewelry insurance and homeowners personal property coverage? It’s your comfort level with risks to your jewelry and the policy coverage limits that may increase those risks.

Does a Homeowners Insurance Floater Cover Jewelry?

The typical standard homeowners insurance covers jewelry to a very limited degree, but a jewelry floater or jewelry rider on an insurance policy is a type of separately scheduled and additional coverage that can protect specifically listed, high-value items like jewelry on a more comprehensive level.

A floater on your homeowners insurance policy, for example, can cover:

- Accidental loss

- Mysterious disappearance

- Accidental damage

However, there are several issues to consider with jewelry floaters. Coverage is not universal: Some floaters or endorsements may still exclude certain types of loss, or define mysterious disappearance differently, so you cannot assume all three items are always covered without checking the actual wording. For example, some insurers may cover “all risk/open perils,” while others may cover only “named perils,” listing specific exclusions. If you make a jewelry claim, those claims will still count against your overall homeowners insurance policy. Additionally, coverage may be limited when you take the jewelry out of the home.

Before opting for a homeowners insurance floater for jewelry, check the policy’s:

- Limits to floater coverage

- Covered peril wording

- Valuation stipulations

- Deductible requirements

What Does a Homeowners Insurance Floater or Rider Not Cover?

Even with a floater, though, jewelry and valuables coverage limits on home insurance still exist, with a floater failing to cover wear and tear, incidents that occur during travel, and more, depending on the carrier.

Common policy limits and restrictions include:

- Mysterious disappearance

- Wear and tear

- Travel

- Maintenance

- Damage due to neglect

When reviewing a jewelry floater/rider, look for phrases like “actual cash value” (which means the policy will pay out what the jewelry is worth, including depreciation, not what it will actually cost to replace the jewelry); “mysterious disappearance excluded”; “we may repair or replace” (which means the insurer can choose the replacement on your behalf); or “deductibles still apply.”

And remember — any jewelry claim on a floater/rider will be officially connected to your homeowners policy, which can impact your overall claims history or future homeowners premiums.

BriteCo’s policy covers of the appraised value.

%

How Limited Is Standard Homeowners Insurance for Jewelry?

When it comes to whether or not homeowners insurance covers jewelry and other certain valuable items, it’s important to realize that most standard homeowners insurance policies have a strict “sub-limit” for jewelry theft, often capping payouts between $1,500 and $2,500 regardless of the item’s actual value.

Beyond this low limit, a standard homeowners policy also typically only covers specific “named perils” like fire or theft, while excluding common issues like accidental loss or a stone falling out of a setting. And an HO policy “can be quick to deny a claim for an intrinsic defect or wear and tear, whereas a specialty jewelry policy will favor you in any ambiguous damage situation,” Redmond says.

Whether alone or paired with an insurance rider for jewelry, standard homeowners jewelry coverage limits mean that most jewelry owners are left vulnerable.

Before making a personal property coverage decision, fully review our side by side comparison.

What Are the Hidden Costs of Putting Jewelry on Your Homeowners Policy?

You may initially think you are getting better jewelry coverage by purchasing a rider or floater on your existing homeowners policy, but there’s a hidden cost to this: Any jewelry claim you make will likely be associated with your primary homeowners policy, which could result in higher overall home insurance rates in the future or even a non-renewal of your policy by the insurance company.

Even if you decide to switch to a new insurance agent or carrier, claims are recorded in insurance industry loss-history databases like CLUE and A-Plus, so your claims history will follow you. “The databases can retain those records for up to seven years,” Redmond says. In some cases, even one claim can prevent you from getting a competitive quote from another carrier should you look for other homeowners insurance providers.

Increased Premiums and Future Non-Renewal

Homeowners claims and renewal risk unfortunately go hand in hand.

Each time you file an insurance claim, that claim is recorded in industry databases that then inform insurers as to the risk you pose, causing them to increase your premiums accordingly. As such, using your jewelry rider or floater could effectively financially penalize you. In some cases, if an insurer sees you have jewelry claims on your policy, they could decide not to renew your policy in the future.

Coverage Limitations and Requirements

Furthermore, given low coverage limits, and other restrictions of a rider or floater, you could still end up spending additional money on jewelry coverage anyway. For example, you might need to still purchase a travel insurance policy, so your jewelry is protected during trips. You might also still need to pay for repairs, if damage occurs that doesn’t fall within your coverage parameters.

File claim through a homeowners standard policy or through a homeowners rider or floater.

Claim reported to loss history databases such as CLUE or A-PLUS. Claim stays on your record for years.

Homeowners Insurance company checks your claim record to assess your risk and set your premium cost.

Your homeowners premium increases 20% since you assessed risk has increased due to an additional jewelry claim.

Your homeowners policy is non-renewed (cancelled) because you have too many claims on your record.

Potential Impact of Filing a Jewelry Claim Through HO Policy

Will a Floater Claim Raise Your Homeowners Premium or Risk Nonrenewal?

Yes, claims can affect premiums and making a jewelry claim when you have a floater or rider affects you just like making a claim on your overall homeowners policy might; you may pay more in premiums later or lose coverage altogether.

If you have to file a claim on your homeowners insurance policy rider or floater, for lost or stolen jewelry, be sure to ask these questions:

- What is the deductible amount I will have to pay if I make a claim?

- What is the limit of my payout for claiming a lost or stolen piece of jewelry?

- How could a jewelry claim affect the cost of my homeowners/renters insurance?

- Could one jewelry claim get my HO policy cancelled or non-renewed?

- Can I use the jeweler of my choice to get a replacement piece for my jewelry claim?

What Are the Advantages of Stand-Alone Jewelry Insurance?

Purchasing a stand-alone jewelry insurance policy to protect jewelry can give you greater peace of mind, as this separate policy will offer more comprehensive coverage, ensuring you can have valuable jewelry repaired or replaced in the event of theft, accidental loss, mysterious disappearance, or damage.

Plus, claims won’t impact your home insurance (so long as you purchased your policy through BriteCo, the only specialty jewelry insurance provider that does not report claims to loss history data services).

More benefits of stand-alone jewelry insurance include:

- Protection worldwide

- Low or zero deductibles

- Automatic value updates

- Repairs made with your preferred jeweler

- Replacements of equal or greater value

“Gold and diamond prices can fluctuate wildly,” Redmond notes. “A specialty jewelry policy with coverage extension can protect you even if your item goes up in value during the policy period.”

What Does Stand-Alone Jewelry Insurance Cover That a Rider or Floater Often Does Not?

A home insurance floater or rider will not necessarily cover your jewelry worldwide, and may not cover mysterious disappearance. It may also not give you the full value of your piece after a claim — but stand-alone jewelry insurance coverage is designed to fill the gap in all of these instances.

Whether it’s a floater or rider, or specialized jewelry insurance coverage, you can ensure you’re purchasing the most comprehensive coverage by checking for the following when comparing plans:

- Does the policy cover accidental loss?

- Accidental damage?

- Mysterious disappearance?

- Theft?

- Claims made while traveling?

- The full value of your jewelry?

While a jewelry insurance floater or rider may protect you more so than the average homeowners policy, for claims that won’t impact your premiums and the most comprehensive coverage, you’ll want a specialized jewelry insurance policy. (More questions? Check out our full guide to how jewelry insurance works.)

When Should You Choose Specialized Jewelry Protection Over an Endorsement?

If you’re still not sure which of these coverage options is right for you, here are a few clues that might key you into the best way to insure jewelry, based on your specific circumstances.

| If this describes you… | Choose this… |

|---|---|

| You have a high-value jewelry collection. | Specialized jewelry insurance that ensures you have enough protection. |

| You frequently wear jewelry outside the home. | A specialized jewelry insurance policy that includes worldwide coverage. |

| You’re worried about claims affecting your home insurance policy. | A separate, specialized jewelry insurance policy. |

| You only need minimal coverage for a modest, lower-value jewelry collection. | Check out your rider or floater options with an insurance professional. |

- For high-value, antique, or sentimental pieces, you’ll often only get enough coverage via a specialized jewelry insurance policy.

- Extra coverage on your homeowners policy may not protect you while traveling.

- Claims on a jewelry rider or floater can impact your homeowners policy premium in the future.

What You Need to Get Covered by Specialized Jewelry Insurance

- Your receipt for the piece of jewelry

- An appraisal (if required by the insurer)

- Photos of the piece from all angles

- A description of the piece

Jewelry Insurance vs. Homeowners Floater FAQs

Is jewelry part of home insurance?

Most standard home insurance policies include very limited coverage for jewelry, often not paying out enough to replace it. A rider or floater can provide additional coverage.

Is it better to insure jewelry separately?

For those with a collection of high monetary or sentimental value, stand-alone jewelry insurance will provide more comprehensive coverage and is often well worth the minimal cost.

If I make a claim on a jewelry rider or floater, will my homeowners premium go up or could I get dropped?

Yes, if you make a claim on a jewelry rider or floater, it could result in your homeowners premium going up or you could be dropped by your insurer.

What insurance do you need for jewelry?

Stand-alone jewelry insurance from a specialized provider is often the best, most comprehensive coverage. It will cover accidental damage, mysterious disappearance and loss, theft, worldwide and more.

Is a homeowners rider or floater cheaper than buying stand-alone jewelry insurance?

Not really. Often, the two will cost about the same per year. In the case of BriteCo, specialty jewelry insurance is often more affordable, with better coverage and less risk.

Don’t put your homeowners policy (or your jewelry!) in peril by relying on a rider or floater for coverage. Get your quote for specialized jewelry insurance now, for protection that gives you greater peace of mind.

Related Article:

How Much Does Jewelry Insurance Cost?

Quiz:

The Engagement Ring Calculator You’ve Been Searching For and it’s FREE!

UP NEXT: Brooches Are Back! How to Style the Accessory for Modern Times

Author