A new fine jewelry purchase is a huge deal, and there are different avenues for protecting your investment. On the one hand, you may be offered a warranty (as a courtesy or added-on costs to your overall purchase) of some kind for your jewelry or watch purchase. On the other hand, there’s insurance to consider for additional coverage. Understanding the differences between a jewelry warranty and jewelry insurance will help you best protect your investment and precious jewelry.

What You Will Learn

What is a Jewelry Warranty?

There are all different kinds of warranties (and sometimes more costs to get a warranty). Generally speaking, a warranty is an agreement put forth by the original manufacturer or retailer. For instance, your engagement ring, wedding ring, earrings, or luxury watch might come with a manufacturer’s warranty with a conditional statement of quality, enduring for a set period of time beginning with the day you purchased the item. Jewelry warranties do vary slightly, but they all state the registration terms. Registration terms will list any standard exclusions, the fine print of coverage, and the duration of protection. Some warranties last for several months to a year (or a number of years) while others are sold as “Lifetime” warranties (more on those later). In any event, you may also receive a “warranty card” with your fine jewelry purchase outlining the terms of your coverage, any associated costs, and exclusions.

What's Not Covered By a Jewelry Warranty?

Alternatively, there’s a longer list of items not covered by a typical jewelry warranty:

- Wear and tear

- Bent or missing prongs

- Discoloration from outside agents

- Bent/misshapen bands

- Loss of a stone/pearl/backing

- Broken clasps or missing links

- Repairs or maintenance done outside the original seller

- Theft

- Transfer of ownership

Depending on the jewelry you’ve purchased, many fine jewelers offer something called a “Lifetime Limited Warranty” to the original purchaser or party to purchase (if the item is gifted) for as long as they own their jewelry. Just like a shorter warranty, a lifetime warranty typically will remain in effect as long as certain conditions are met, including but not limited to:

- Regular cleaning/inspection by the original seller at set intervals

- All repair work is performed by the original seller

- Warranty only valid with the original owner – Not transferable

If you find yourself still questioning what is and is not included in your jewelry warranty, please go to the original seller or the manufacturer. Warranties can vary, and it is a risk to not fully understand the protection you may or may not have. Some warranties may have a deductible, cover basic maintenance, or help pay for repairs. If you were gifted jewelry, like an engagement ring, it is important to find out if there is a manufacturer’s warranty, extended warranty, or jewelry warranty for your gift and understand what is covered or not in case anything happens.

What is Jewelry Insurance?

Even if you have a solid jewelry warranty, you need to properly insure your jewelry. A jewelry insurance policy usually refers to a specific policy meant to cover an engagement ring, wedding band, earrings, or luxury watch. It will protect the policyholder in the event of perils such as:

- Damage

- Loss

- Theft

- Mysterious Disappearance

A jewelry insurance policy usually doesn’t cover things that your jewelry warranty does, like manufacturing defects. In some cases, you may be able to find jewelry insurance that covers preventative maintenance to protect your pieces from wear and tear. This means an insurance company wants to ensure your personal belongings not only look their best but also will cover the cost of tightening prongs, sealing bezels, and maintaining sturdy clasps for normal wear.

As with warranty coverage, several different types of jewelry insurance coverage are available in the marketplace, ranging from generic “Personal Articles” policies (that aren’t technically specific to jewelry) to iron-clad, specialized jewelry or watch insurance policies like those offered by BriteCo. Another added bonus to obtaining a jewelry insurance policy is most do not have a deductible and also helps protect your renters or homeowners policy if you have to file a claim.

Insuring With Your Homeowners Policy

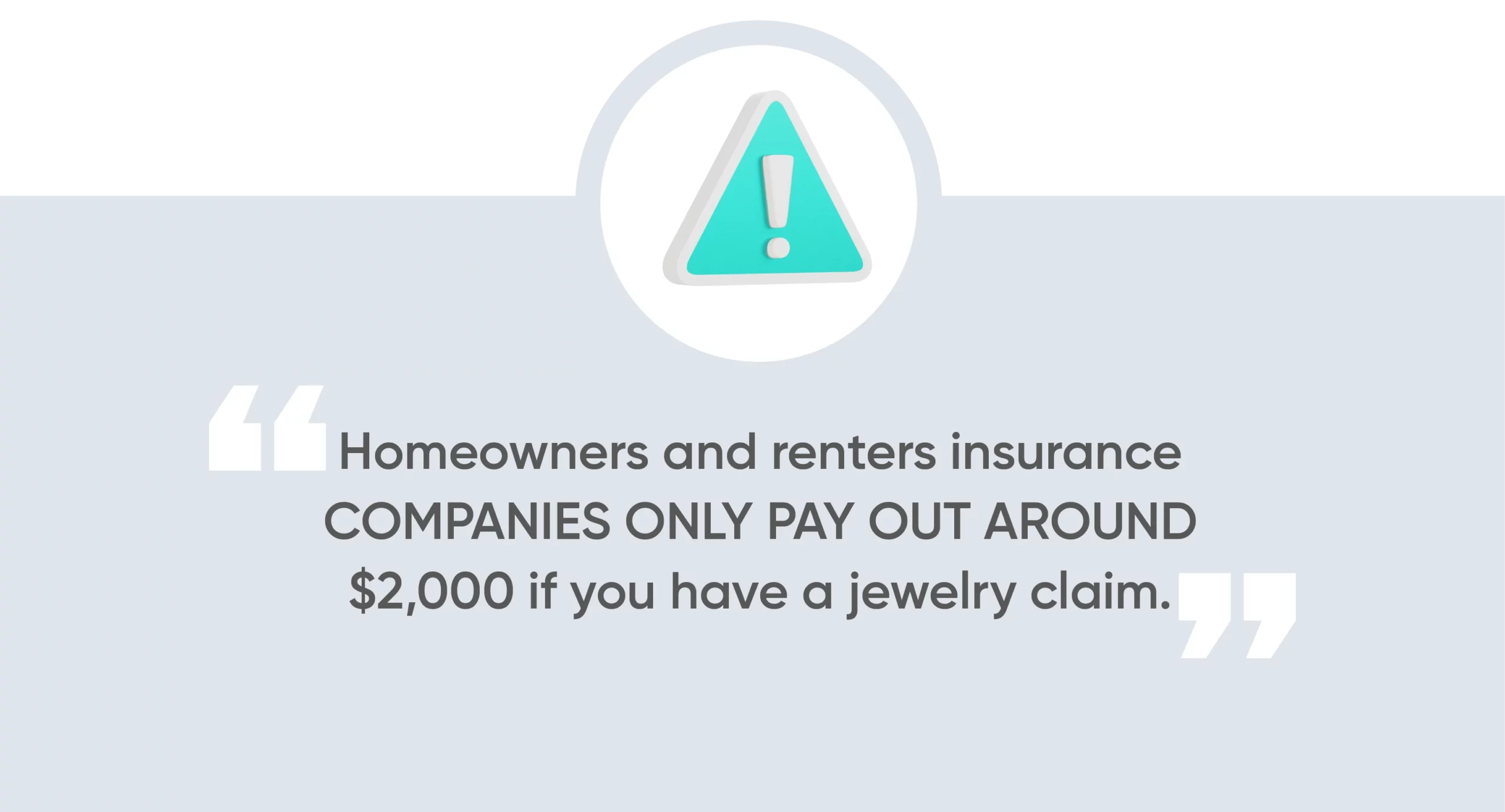

Does homeowners insurance cover jewelry? If you have a basic homeowners insurance or renters insurance, your first instinct might be to list your jewelry on the policy to provide financial protection for your personal belongings. However, if the value of your jewelry exceeds $1,000 to $2,000 per item, you’ll definitely want a specialized policy just to cover your jewelry (more on that below). This is because most homeowners and renters insurance companies only pay out around $2,000 if you have a jewelry claim, no matter how much your jewelry is actually appraised for (learn more about jewelry appraisals here). Most believe their home insurance policy offers complete protection of their jewelry items when really there are hard limits to what they do cover and what they pay out.

One out-of-pocket cost involved with most homeowners or renters policies is the deductible or the amount of money you’ll need to pay upfront toward filing a claim on your valuable items. In general, the types of claims you’ll be able to file against your homeowners or renters policy will be directly related to theft. Certain claims against damage, and most claims involving – instances where the item isn’t necessarily stolen, but it’s certainly lost without recourse – are not honored by most homeowners and renters insurance policies. In simpler terms, you would cover the cost of repairs and even the replacement of your stolen or lost item, even if you were covered by your homeowners because of their limits.

When you think about it, you rely on your homeowners policy to also cover the physical dwelling you live in, plus everything inside it. If you have a jewelry claim, it could cause your homeowners rates to increase. And if you ever have to make an additional property damage claim against your policy down the line, you could risk getting canceled because of your prior jewelry loss – because you insured everything on the same policy. Thankfully, there’s a better option for insuring your valuables.

Shopping for Specialized Jewelry Insurance

When it comes to shopping for an insurance policy to cover your precious valuables, it might be best to consider insuring with a dedicated jewelry insurance provider, especially if you own fine jewelry valued above $2,000. When shopping for carriers, look at the difference in their coverage limits, deductibles, and how they pay or replace your item in the event of a claim.

At BriteCo, we provide the industry’s most comprehensive, worldwide coverage against loss, damage, theft, and mysterious disappearance. BriteCo jewelry insurance policies also include provisions for routine maintenance, such as prong tightening, to ensure your engagement ring or wedding ring remains intact. BriteCo offers all of this, plus automatic coverage of up to 125% of the appraised value of your jewelry at no extra charge, all with a zero-dollar deductible.

We hope this comparison between jewelry warranties and jewelry insurance helps paint a clearer picture of what each type of protection involves. Even if you have a warranty, you’ll need to properly insure your fine jewelry. BriteCo makes it super easy to obtain a straightforward, easy-to-understand jewelry insurance quote. You can check your price today and get covered in no time!

Related Articles:

Carat vs Karat? | BriteCo Jewelry Insurance

Understanding The Different Types of Clasps For Jewelry

Rare Carat Ring Insurance

Jared Ring Insurance Protects Your Precious Pieces

Shane Co Ring Insurance

How Much Does Jewelry Insurance Cost?

Appraisal Tool:

The Easiest Way to Get a Professional Jewelry Appraisal Valuation!

UP NEXT: How to Remove a Link from a Jewelry Chain Bracelet

Author