Getting a jewelry appraisal for insurance purposes is important for one key reason: Insurers need an appraisal or other strong documentation of value to understand what your jewelry would cost to replace today, and thus ensure you have proper jewelry insurance coverage.

Some insurers will accept a detailed sales receipt in lieu of an appraisal for newer pieces, but older, inherited, custom, or upgraded jewelry usually needs a new, proper appraisal.

With some guidance from BriteCo Chief Actuary Conor Redmond, let’s take a look at the need-to-know details, such as:

- Why insurers need proof of value

- When a receipt may work vs. when you need an appraisal

- Where to get jewelry appraised

Plus, we’ll discuss how valuation works and what makes an appraisal most useful for insurance, such as added documentation including detailed receipts and lab certificates.

What You Will Learn

- Do I Need an Appraisal for Jewelry Insurance?

- Valuation of Jewelry for Insurance

- What Counts as a Good Jewelry Appraisal for Insurance?

- When a Receipt Can Work Instead of an Appraisal

- Where to Get Jewelry Appraised

- Expert Tips for Getting an Accurate Appraisal

- How Much Does a Jewelry Appraisal Cost?

- How Often Should You Update an Appraisal for Insurance?

- What You’ll Need to Apply Once Your Appraisal Is Ready

- FAQs About Jewelry Appraisal/Insurance

- Jewelry Appraisal for Insurance: Quick Recap and Next Step

Do I Need an Appraisal for Jewelry Insurance?

You usually need an appraisal or other strong proof of value to get jewelry insurance, but the specific necessary documentation can depend on the age, type, and past documentation quality of the piece.

Unsure if you need a jewelry appraisal for insurance?

- Is the piece of jewelry new and well documented? If so, a receipt may work for insurance purposes.

- Has the jewelry been upgraded, inherited, or changed? Get an appraisal.

- Are you unsure if an existing appraisal reflects the piece’s current value? Update the appraisal before getting an insurance quote.

Valuation of Jewelry for Insurance

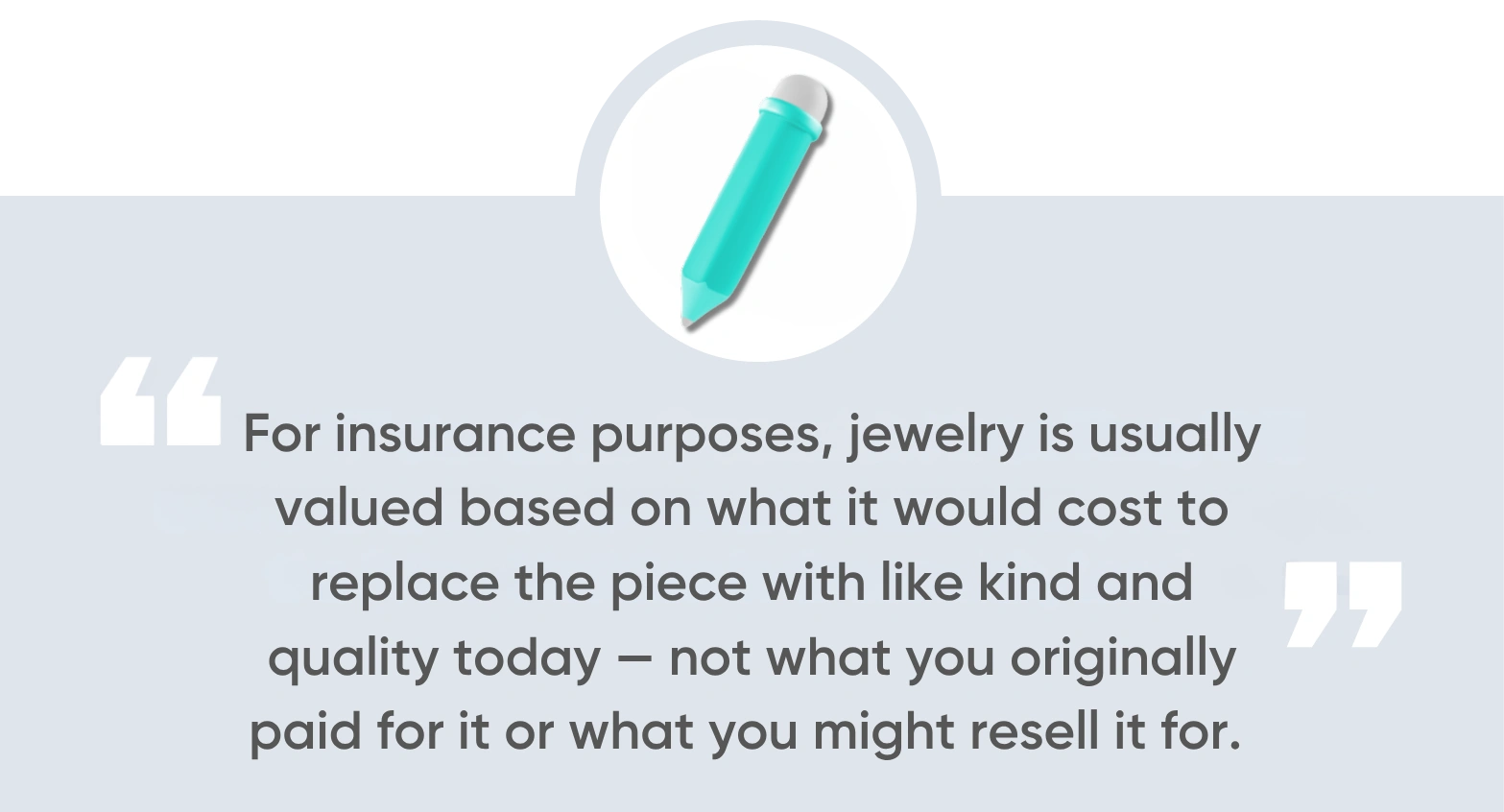

For insurance purposes, jewelry is usually valued based on what it would cost to replace the piece with like kind and quality today — not what you originally paid for it or what you might resell it for. “It is essentially a defensible estimate for the cost to replace the item with like kind and quality over a certain time horizon, like one to two years,” Redmond says. “It is typically very close to the retail value.”

Key factors that might determine a piece’s retail replacement value include:

- Metal type and weight

- Gemstone quality and current value

- Craftsmanship and/or design complexity

- Market value

Due to these factors, insurance valuation can change over time, even when the jewelry itself has not.

Replacement Value vs. Fair Market Value vs. Liquidation Value

Replacement value is usually the number insurers care about most, while fair market value and liquidation value are used for other situations.

| Different Valuations | What It Means | When It’s Useful |

|---|---|---|

| Replacement Value | What it costs to replace a piece of jewelry today with like kind and quality | For insuring jewelry |

| Fair Market Value | What a buyer and seller will willingly agree to in the open market | During resale, estate planning, or divorce settlements |

| Liquidation Value | What the piece might sell for quickly | Forced-sale conditions |

“Sometimes, when purchasing a used or discounted item, the replacement value can be significantly higher than the purchase price,” Redmond says.

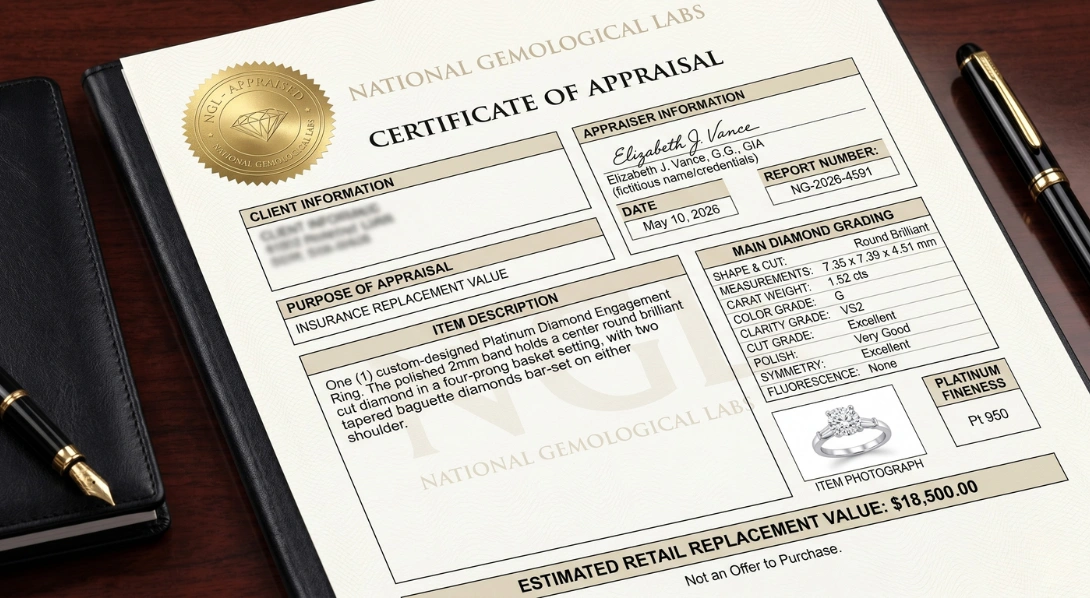

What Counts as a Good Jewelry Appraisal for Insurance?

A good jewelry appraisal report will clearly identify the item and give a replacement value that an insurance company can then use for coverage.

Before applying for jewelry insurance coverage, ensure that your appraisal includes:

- The appraiser’s name and business name

- Date of the appraisal

- Detailed descriptions of appraised items

- Stone and metal details, such as carat weight, quality, and/or clarity

- Photos of appraised jewelry items

- Clearly stated appraised value

Keep in mind that if your appraisal reflects too little information, or is vague and older than a few years, it’s more likely to create friction later, if you try to acquire jewelry insurance or make a claim on an existing insurance policy.

When a Receipt Can Work Instead of an Appraisal

A detailed sales receipt can sometimes work instead of an appraisal for a newer piece, but only if it clearly documents what the item is and what it cost.

“For watches, receipts are typically fine,” Redmond says. “An insurer will accept a receipt if there are sufficient details to determine like kind and quality. For example, on a mass-produced item with an SKU inventory code, a receipt would be an acceptable form of documentation.”

An insurer also may accept a receipt in lieu of an appraisal if:

- The piece of jewelry was a recent purchase

- The jewelry store provided detailed documentation for the piece

- The receipt clearly shows the price you paid

However, an insurer may not accept a receipt in lieu of an appraisal if:

- You inherited the piece

- The piece was upgraded after purchase

- The receipt is vague or incomplete

- The piece is in an unclear condition or has an unclear value

So, do I need an appraisal to get jewelry insurance? If your receipt does not meet the correct standards that insurers expect for fine jewelry, then, yes, you need an appraisal.

Where to Get Jewelry Appraised

When it comes to deciding where to get jewelry appraised for insurance, the best option will be with a local qualified jewelry appraiser or reputable jeweler, an independent professional jewelry appraiser, or online appraisal services, if your piece is straightforward and well-documented.

When getting jewelry appraised for insurance, the best fit will be:

- A local qualified professional if you want to prioritize convenience

- An independent certified appraiser with a specialty if you have a unique piece

- An online appraisal services provider, if you want the fastest option

BriteCo’s online jewelry appraisals come as a certified PDF delivered by email for $26. At the time of appraisal, BriteCo will also determine whether or not your item is suited for an online valuation, or if you need to find a local appraiser for an in-person inspection.

What Credentials Should You Look for in an Appraiser?

A strong insurance appraisal is more trustworthy when the appraiser has relevant gemological training and recognized professional affiliations.

Look for credentials such as:

- Continuing education certifications from the Gemological Institute of America or a similar national association

- Membership in recognized appraisal organizations such as the NAJA, ASA, or ISA

- Evidence of current practice and work that follows accepted industry standards

Expert Tips for Getting an Accurate Appraisal

The best way to get an accurate insurance appraisal is to show up with the best possible documentation and the clearest possible description of the valuable pieces you wish to have appraised.

- Bring any original receipts or prior appraisals.

- Provide any grading reports that you may have.

- Mention any repairs, upgrades, or custom work that was done to the piece.

Providing this information matters especially for engagement ring upgrades, heirlooms, and other valuable pieces in your collection where the current replacement value may not match older paperwork.

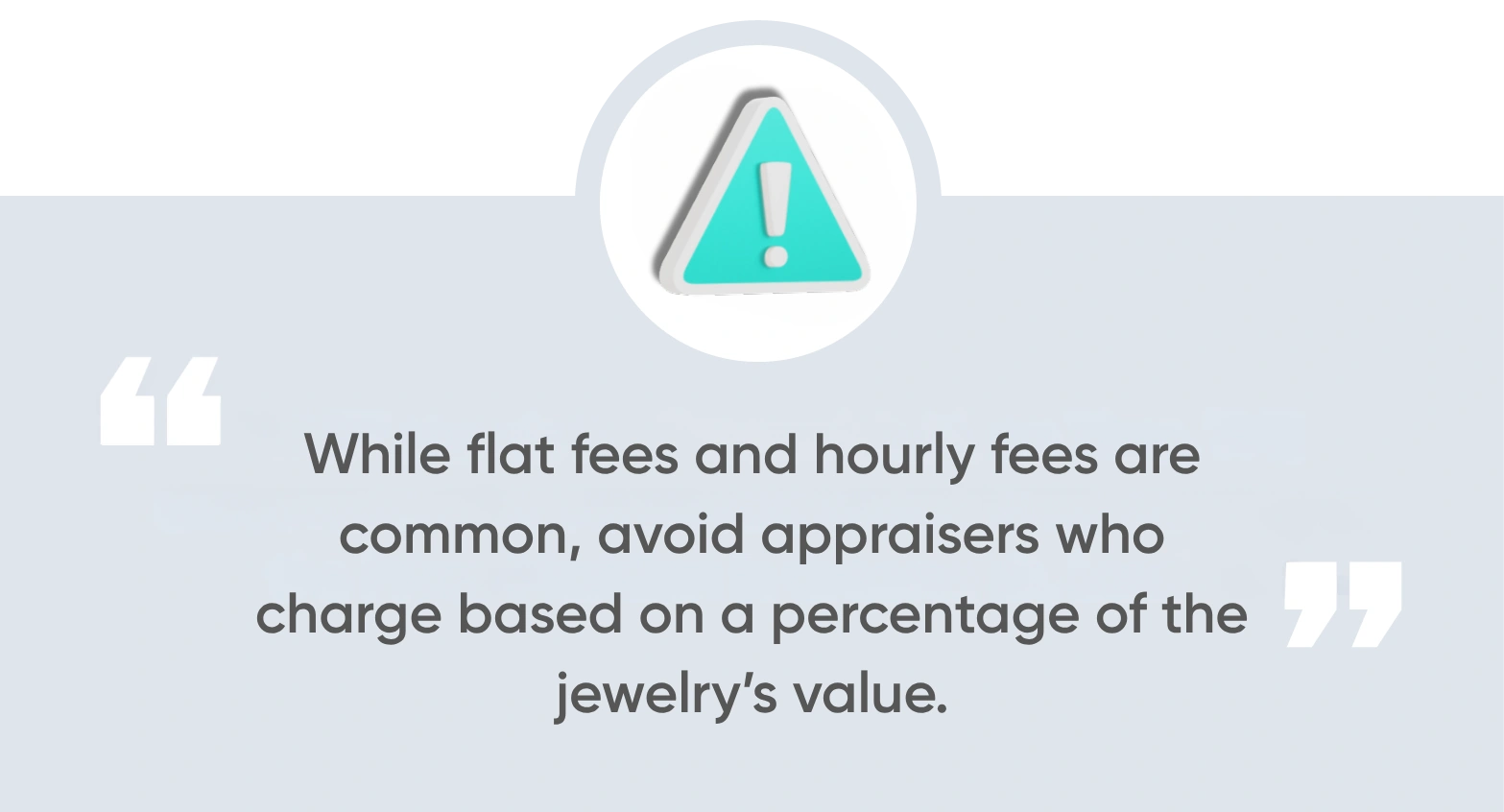

How Much Does a Jewelry Appraisal Cost?

A jewelry appraisal fee will vary depending upon the appraiser you choose, the complexity of your piece, and whether or not the appraiser charges by the item or by the hour.

So, how much does jewelry appraisal cost?

- Common appraisal flat fees are $50-$150 per item

- Detailed insurance appraisals may average $100-$125

- Appraisals for more intricate or high-value pieces may exceed $200

- Hourly rates, meanwhile, hover around $50–$150

BriteCo’s current online appraisal option starts at $26 for eligible pieces.

While flat fees and hourly fees are common, avoid appraisers who charge based on a percentage of the jewelry’s value.

How Often Should You Update an Appraisal for Insurance?

As a rule of thumb, you should get your jewelry appraised as a part of your regular maintenance, so that the value of your jewelry is accurately reflected by your insurance coverage — about every three years, or sooner if there are major market changes or you upgrade the piece.

As such, regular appraisals should be scheduled for every three years, but other factors that mean you need an appraisal sooner include:

- If the piece has been reset or upgraded

- If you inherited the piece

- If the value simply feels outdated

- If the insurer requests an update

If the paperwork no longer reflects today’s replacement value, it can create avoidable friction when coverage or claims are reviewed. Learn what to expect with ring appraisals and more about how quickly you’ll need to schedule your next appraisal.

What You’ll Need to Apply Once Your Appraisal Is Ready

Once your appraisal is ready, getting comprehensive coverage via a specialized jewelry insurance policy is usually just a matter of submitting proof of value, current photos, and basic item details to insurance providers.

Jewelry insurance application checklist:

- Updated jewelry appraisal or detailed receipt

- Jewelry photos

- Basic jewelry details

- Any supporting reports, such as gemstone grading reports

When you’re ready, learn more about how does jewelry insurance work.

FAQs About Jewelry Appraisal/Insurance

Do I Always Need an Appraisal to Get Jewelry Insurance?

While getting a jewelry appraisal and insurance often go hand in hand, you may not need an appraisal if the piece is new and you have sufficient documentation. However, any other valuable pieces do typically need an appraisal, to ensure appropriate coverage.

Can a Receipt Work Instead of an Appraisal?

If you have a receipt for a recent purchase that clearly shows the cost of your jewelry, you may be able to use that for insurance purposes, rather than having to pay for a new appraisal.

What Does “Valuation for Insurance” Mean?

Valuation for insurance refers to how much it would cost to replace your item today, with like kind and quality. This differs from fair market value and liquidation value, which are more appropriate for estate planning, divorce settlements, or if you want to sell an item and need to know how much a buyer might be willing to spend.

Where Should I Get Jewelry Appraised?

Get your jewelry appraised by a certified appraiser, either locally or online, with credentials that align with industry standards, such as certification from continuing education programs.

Are Online Jewelry Appraisals Accepted?

Yes, you can have your jewelry appraised via a credible online appraisal provider, and your insurance will likely accept it.

Jewelry Appraisal for Insurance: Quick Recap and Next Step

Getting jewelry insurance usually starts with being able to show proof of value, and the strongest proof is a current appraisal that clearly states your items’ replacement values.

If you don’t have an appraisal yet, the simplest next step is to find a local appraiser, or use BriteCo’s online appraisal services, for eligible pieces. BriteCo’s current online service is $26 for qualifying items.

Related Article:

Quiz:

The Engagement Ring Calculator You’ve Been Searching For and it’s FREE!

UP NEXT: How to Remove a Link from a Jewelry Chain Bracelet

Author