Hosting an Event at Home? Consider Private Event Insurance

Home is where the heart is — and where many events are. What better place to feel comfortable and at ease? But before you host a bash at your place, or someone else’s, be sure to protect the space.

Private event insurance is basically event liability insurance that protects you against any financial losses if a personal injury or damages were to occur during the course of an event. As such, insurance for private events is a necessity when hosting a wedding or other gathering at a private residence, whether it’s your own home, a friend or family member’s home, or a rental.

Here’s what you need to know about how private event liability insurance works, as well as private event insurance cost, how to get a policy, and more.

What You Will Learn

- Private Party Event Insurance for Your Own Home

- Other Things to Consider With At-Home Special Event Insurance

- Private Event Insurance for Someone Else’s Home

- Airbnb Event Insurance and Vrbo Event Insurance

- Final Considerations for At-Home Events

- Can You Get Event Cancellation Coverage?

- Wedding and Event Insurance FAQs

- Insure Your At-Home Wedding or Special Event with BriteCo!

Private Party Event Insurance for Your Own Home

Hosting a special event at home is typically cheaper and easier than renting a full venue. It’s why many couples, particularly Millennials and Gen Z, are choosing backyard weddings over more traditional venues. However, the cost can really add up if something goes wrong and you don’t have the right backyard wedding insurance.

Or maybe it’s a baby shower, or family birthday parties, or bat mitzvahs you’re setting up at home. If you’re hosting a large special event of any kind on your personal property, you’ll want to consider home event insurance to fill in the gaps with your existing home insurance policy.

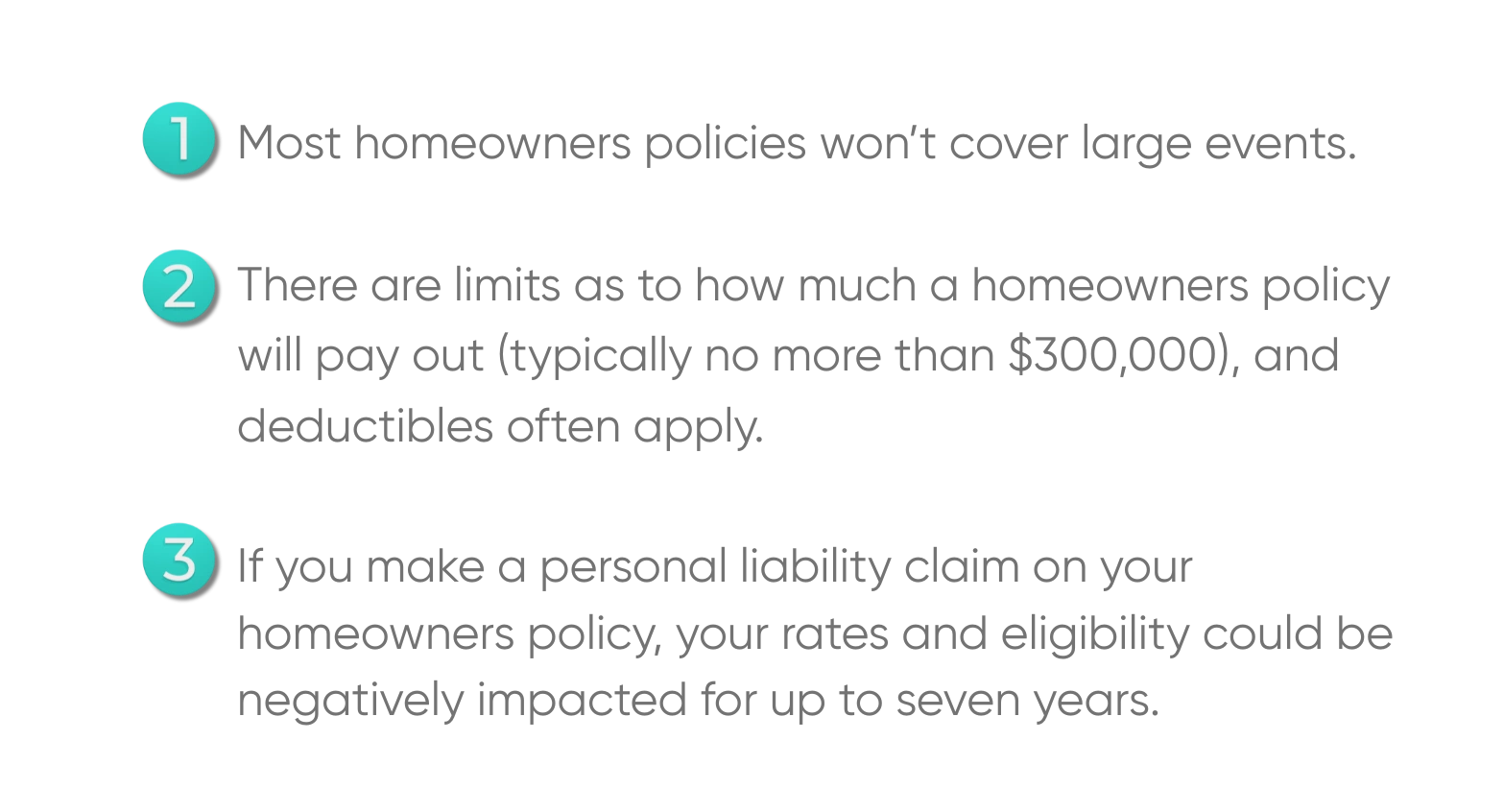

Your Existing Homeowners Insurance Won’t Cover Large Events

Your existing homeowners insurance likely does provide some personal liability coverage for events, but there are some substantial exceptions and gaps:

In contrast, specialized insurance for weddings at home provides higher liability limits, lower deductibles, and considerations that are specific to a one-day event.

In contrast, specialized insurance for weddings at home provides higher liability limits, lower deductibles, and considerations that are specific to a one-day event.

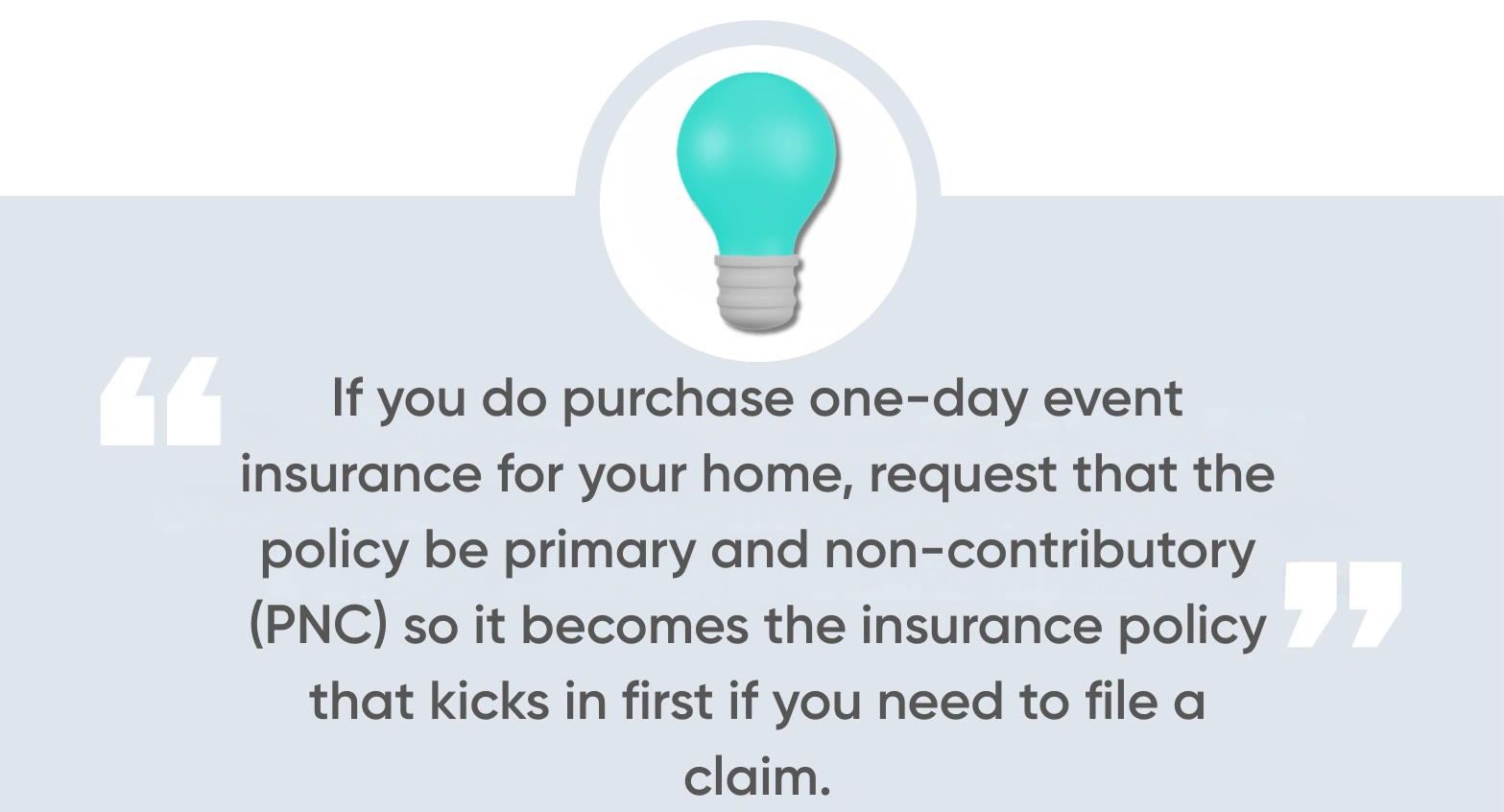

Pro tip: If you do purchase one-day event insurance for your home, request that the policy be primary and non-contributory (PNC) so it becomes the insurance policy that kicks in first if you need to file a claim.

Other Things to Consider With At-Home Special Event Insurance

When shopping for single-day event insurance, you’ll also want to keep in mind the nuances surrounding Med Pay limitations, guest-caused property damage, contract requirements, and insurance requirements, especially if you’re serving alcohol at the event.

Medical Payments (Med Pay)

While Med Pay coverage on your existing homeowners policy may cover you if an injury occurs during an event, the payout limit is very low — about $2,000 at most. For more comprehensive coverage, you’ll want to add No Fault Medical Payment coverage to your specialized event liability insurance.

Guest-Caused Property Damage

If a guest damages your personal property, your one-day event insurance will not cover those associated costs. Instead,you would rely on your existing homeowners insurance.

However, in case a guest damages rented items for the event, rather than your own property, you probably want to have separate special event insurance. But you can also check your current homeowners policy to see if you’re covered in this instance.

Written Contracts

You do not need a written contract if your insurance coverage only applies to bodily injury liability.

Host Liquor Liability Coverage

Both your homeowners insurance policy and your one-day event insurance will cover host liquor liability if you’re serving alcohol at your function. However, neither will cover you if it’s a professional bartender that’s doing the serving. In this case, the vendors or business that’s hired should have their own coverage.

Private Event Insurance for Someone Else’s Home

Let’s say you’re not hosting your event at your own home, but rather at a family member or friend’s residence — in this case, the property owner’s existing homeowners policy may protect them under certain circumstances, but it won’t directly protect you.

For example, if personal injury occurs on the property during the event, the homeowner may be covered, but if you were named in a lawsuit as the event host, you would have none of your own coverage and would still be liable for any claims made against you.

To avoid this very costly and potentially devastating situation, you should purchase specialized private event insurance, adding the private home/homeowner to the policy as additional insureds.

Again here, make sure the policy is primary and non-contributory (PNC), so it’s used first, before the homeowner’s policy. Additionally, consider buying medical expenses coverage, which can immediately pay for any necessary treatment for guests.

Other Things to Consider When Hosting at Someone Else’s Home

Another option to help the event go smoothly is to ensure your policy will cover damage to the homeowner’s property, so you’re not left with a tense situation if a rowdy guest breaks a window or runs over the mailbox. It’s also strongly recommended to have a written contract between you and the homeowner, including details about not only insurance, but also the maximum number of guests allowed, the plan for serving alcohol, who’s held responsible for cleanup, etc.

Airbnb Event Insurance and Vrbo Event Insurance

If you’re hosting a wedding at an Airbnb or Vrbo property, purchasing a specialized event insurance policy is also critical for a few key reasons:

- Host protections provided by platforms like Airbnb do not typically cover special events.

- The actual homeowners liability insurance may likewise not cover special events.

- Your own homeowners policy will not protect you at someone else’s private residence.

As such, you’ll want to purchase a stand alone, special event insurance policy for your rental home event, which will cover bodily injury and any property damage, as well as liquor liability for any alcohol served. (Remember that this only applies if you are serving the alcohol; a professional bartender needs their own coverage.)

Just as you would when hosting a wedding at someone else’s home, ensure the policy includes primary and non-contributory wording and add the rental homeowner as an additional insured. If the rental owner requests it, you might also include a waiver of subrogation, which means you can’t sue them if an incident occurs.

Final Considerations for At-Home Events

There’s one more important item you’ll want to keep in mind when having an at-home event: hiring licensed and insured vendors.

Always Hire Licensed and Insured Vendors

This step will help mitigate any potential damage done by a vendor, such as tenting and rentals. The setup and teardown process often involves heavy equipment, which increases the risk of accidental damage. But if anything happens, they have their own insurance policies that will kick in.

Can You Get Event Cancellation Coverage?

Events held at residential locations still qualify for cancellation coverage. All of the policies we’ve talked about offer protection from financial liability in the event of third-party property damage and personal injury, but many find event cancellation insurance to be an equally valuable add-on, as it helps cover lost deposits and similar costs in the event you cancel or postpone your wedding or other at-home event due to situations outside of your control, like extreme weather or infectious disease.

But it’s important to note that cancellation coverage will be the same no matter if you’re hosting your wedding or event at a traditional venue, your own home, someone else’s home, or a home rental.

Wedding and Event Insurance FAQs

How Much Does Event Insurance Cost?

If you want to buy event insurance, you’ll find that most liability policies for weddings and other special events cost just a few hundred dollars, with rates ranging based on factors such as event duration, number of attendees, location, and more.

Do You Have to Buy Event Insurance for a Wedding?

Many venues require proof that you have event insurance before they will allow you to sign a contract and pay your rental deposit. However, even if your venue does not have this requirement, event insurance is still a smart idea, as it can keep you from being 100% financially responsible for bodily injury that may occur during the event.

Will Your Homeowners Insurance Company Cover a Home Wedding?

Homeowners insurance may insure your event to a very small degree, and only if the guest list is very short. Otherwise, and especially if you want to avoid negatively affecting your premium in the event of a claim, special event coverage is necessary.

Does Homeowners Insurance Cover a Cancelled Home Wedding?

No, a homeowners insurance policy will not provide any coverage for a cancelled home wedding. If you want cancellation coverage to help you recoup costs related to cancelling or postponing a wedding, you need to buy a wedding cancellation policy ahead of the big day.

What are the Types of Wedding Insurance?

There are two primary types of wedding insurance: event liability insurance and cancellation coverage.

Insure Your At-Home Wedding or Special Event with BriteCo!

If you only rely on your homeowners insurance to provide coverage for your event, you could be setting yourself up for a big risk. Instead, special event insurance will comprehensively protect you when you’re hosting a wedding or similar gathering at a private residence. Getting a quote takes mere minutes and you may be surprised at how little it costs (sometimes even under $100!). Get started now!

Related Articles:

Can You Rent Jewelry for a Wedding?

What Wedding Insurance Do I Need?

Cute Wedding Outfits for Your Pets

The Best Winter Wedding Colors

How to Postpone a Wedding Due to a Natural Disaster

How to Get Married in Vegas

Perfect Second Marriage Wedding

Affordable Wedding Insurance: More Coverage, Less Cost!

UP NEXT: What You Need to Know about Renting a Photo Booth for Your Wedding

Author